What is LenDeFi protocol (LDFI) | What is LenDeFi protocol token | What is LDFI token

Introducing Lendefi — Redefining the defi space with undercollateralized loans

The Decentralized Finance (“DeFi”) ecosystem has grown exponentially over the past year and has started to unlock a new era for modern day financial products and services. DeFi provides an infrastructure harnessing the power of blockchain solutions to enable robust and modern financial solutions. DeFi products will replace almost all contemporary financial services, including savings, insurance, trading, and loans.

The early innovation in DeFi with multiple major platforms like Compound, AAVE, bZx, have paved the way for the adoption of crypto lending and borrowing. However, the problem with these earlier offerings is they are often overcollateralized and/or targeted towards margin trading, hence intrinsically very inefficient in their usage of capital and creates a barrier to entry for the everyday mum and dad lender or borrower.

Image Source: Loanscan

Therefore it is evident the most compelling use case of DeFi is Undercollateralized Loans (“UCLs”), which are needed now, more than ever before, given the rapid rise of crypto into the mainstream with tech giants such as Facebook and PayPal now participating.

Understanding undercollateralized loans

The simplest way to understand a UCL is by using an analogy to real estate ownership via a mortgage loan. Welcome to the world of UCLs — imagine only putting up that fraction of the house’s value equivalent as a deposit and getting a mortgage to finance the rest instead of paying the entire value of the house yourself. When you wish to cash out the gains from your investment, you can sell the asset and walk away with all the profits after paying the bank the borrowed funds and interest.

Now, imagine taking a loan to purchase a crypto asset such as BTC, ETH, UNI, LINK, AAVE or YFI. Say, for instance, that BTC is worth $20,000, but you only have $10,000 to invest, and would like to purchase a whole BTC rather than half of one. But if you walk into your friendly local bank and ask for a loan to purchase BTC, they will of course, flatly refuse you.

What now? Your more prudent option would be to take out a loan from a blockchain-powered platform that offers UCLs. But who will lend the money to you, and why would they?

The interest that people receive in the traditional banking system is nearly zero, or even going at negative rates in multiple countries, where customers have to pay the bank to hold their money, which is a complete utter fallacy. This leaves people with little, or no secure lending options where they can earn attractive rates of interest on their money. While it is easy for anyone to borrow money from the bank to buy assets like cars and houses, there are few options available for the borrowers to invest in crypto assets. This major gap in the market remains untapped, and Lendefi are bridging this gap in the market.

Introducing Lendefi

The Lendefi protocol (the “Protocol”) allows secured lending, giving the much-needed confidence to the lenders in a highly volatile crypto market. Secure lending options will open up lending opportunities for traditional and private lenders to access higher interest rates without getting direct exposure to the crypto market fluctuations.

Lendefi protocol cuts the middle-man out of the lending process and eliminates the red tape involved with the lending and borrowing. This removes any counterparty risk between the borrower and the lender, who then can deal on a trustless basis.

The lender will receive a variable interest and be secured by the liquidity provided on the DeFi ecosystem in such protocols as Uniswap . Hence, if the borrower is not able to maintain their loan, the Protocol will ensure the lender is repaid and the borrower credited with the remaining equity.

Borrowers can select from a wide variety of supported assets to invest by borrowing funds from the Protocol. Supported assets can be added and removed via Lendefi’s decentralized governance mechanism (the “DAO”).

The base currency for lending and borrowing is USDC, hence making it more user-friendly and fostering mainstream adoption. Lendefi has specifically chosen USDC because it is the safest stable coin from a custody and reputation perspective, given it is a collaboration between Coinbase and Circle, and undergoes regular audits and is subject to regulatory compliance.

How Lendefi works?

From a technical perspective it works like this:

- USDC is lent to the Lendefi smart contract (the “Contract”).

- The Borrower deposits USDC into the Contract and invests in one of the listed digital assets.

- With attractive Loan to Value (“LVR”) rates, the borrower can invest much higher than the equity in the borrower’s deposit, providing leverage.

- Borrowed funds are securely held in the Contract.

- When the crypto asset is sold, the lender’s principal is returned to the lender and the balance remains with the borrower.

Let’s talk security

Security issues have plagued many lending platforms in the DeFi space where exploits related to ‘flash loans’ have been a common occurrence. Platforms are resorting to offering higher yields (see https://defirate.com/lend/) in order to re-attract lenders. In reality these aggressive tactics are a simple case of “high risk = high return”. **_Lendefi _**addresses this issue by escrowing the borrowers investment asset (the “Asset”) within the Protocol itself, therefore negating exploits that allow withdrawal of the Asset by a hacker. The result is less risk for borrowers and lenders, in turn providing further confidence in the Protocol as compared to other DeFi lending platforms.

It may be cliche to say “crypto shouldn’t be cryptic” but it’s so true. Most existing decentralized lending platforms are simply too convoluted for the everyday person to adopt. This is where Lendefi, an innovative DeFi protocol, comes in and provides a solution where it’s as simple as “borrow and invest in crypto” or “lend and earn interest on stable coins”.

As you can see UCLs are not only compelling but highly disruptive to the legacy financial system. Lending sits at the core of the banking system, hence when challenged by UCLs, the ramifications will reach far and wide. With the widespread adoption being witnessed in the blockchain space, the future seems bright for DeFi-powered Undercollateralized Loans.

Tokenomics

LDFI is the native token of the Lendefi protocol (the “Protocol”). LDFI is a governance token which controls the interest rate model, inclusion of supported assets, reward distribution and other terms and conditions and any changes of the Protocol.

Decentralized governance

Lendefi governance via a Decentralized Autonomous Organization (“DAO”) will allow active participation of the token holders in the governance of the Protocol.

Voting

Any address holding over 1% of the tokens or voting right delegated to that address by over 1% of total supply can create proposals and the changes can be made to the Protocol via voting on the DAO.

Fees

The difference between the interest rate the borrower pays and the lender recieves, otherwise know as the spread, will be used to purchase LDFI tokens from the market for the purpose of burning and rewards.

Token burning

Through a process known as burning, LDFI tokens will be burnt, hence lowering the total and circulating supply. This will result in increasing the value of LDFI tokens, therefore creating further value for the token holders.

Rewards

A variety of rewards will be given in order to encourage the growth of the Protocol and creation of value for token holders.

Staking rewards

LDFI token holders will be able to stake their Tokens and in doing so will receive a reward in the form of LDFI tokens.

Liquidity rewards

Lendefi will operate a liquidity rewards program in order to provide rewards in the form of LDFI tokens to liquidity providers on a decentralized exchange where LDFI will be listed, such as Uniswap.

Liquidation rewards

To encourage the liquidation process, liquidators will be provided a reward in the form of a percentage of the collateral being liquidated in the case of borrower default.

Yield farming

In order to foster adoption of the Protocol, lenders and borrowers will be rewarded with LDFI tokens for using the Protocol.

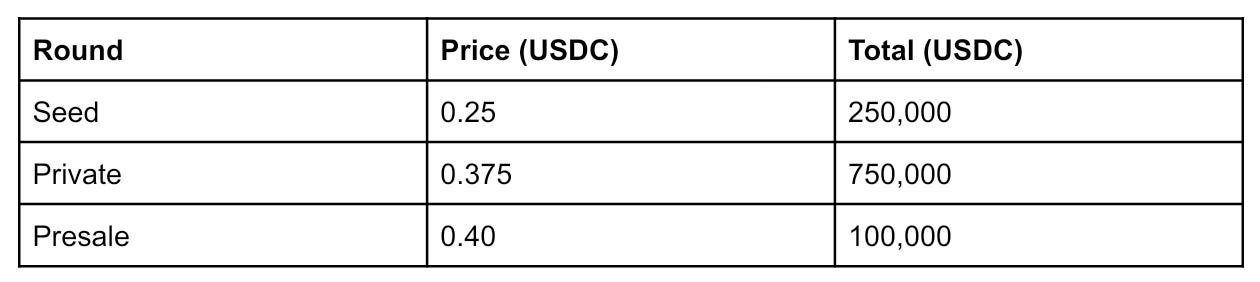

Token Price

Initial circulating supply

Approximately 1,800,000 LDFI Tokens

(2,150,000 LDFI including Locked Liquidity Provisioning)

Initial market capitalization

Approximately 720,000 USDC

Uniswap liquidity provisioning

500,000 LDFI | 200,000 USDC (equivalent in ETH)

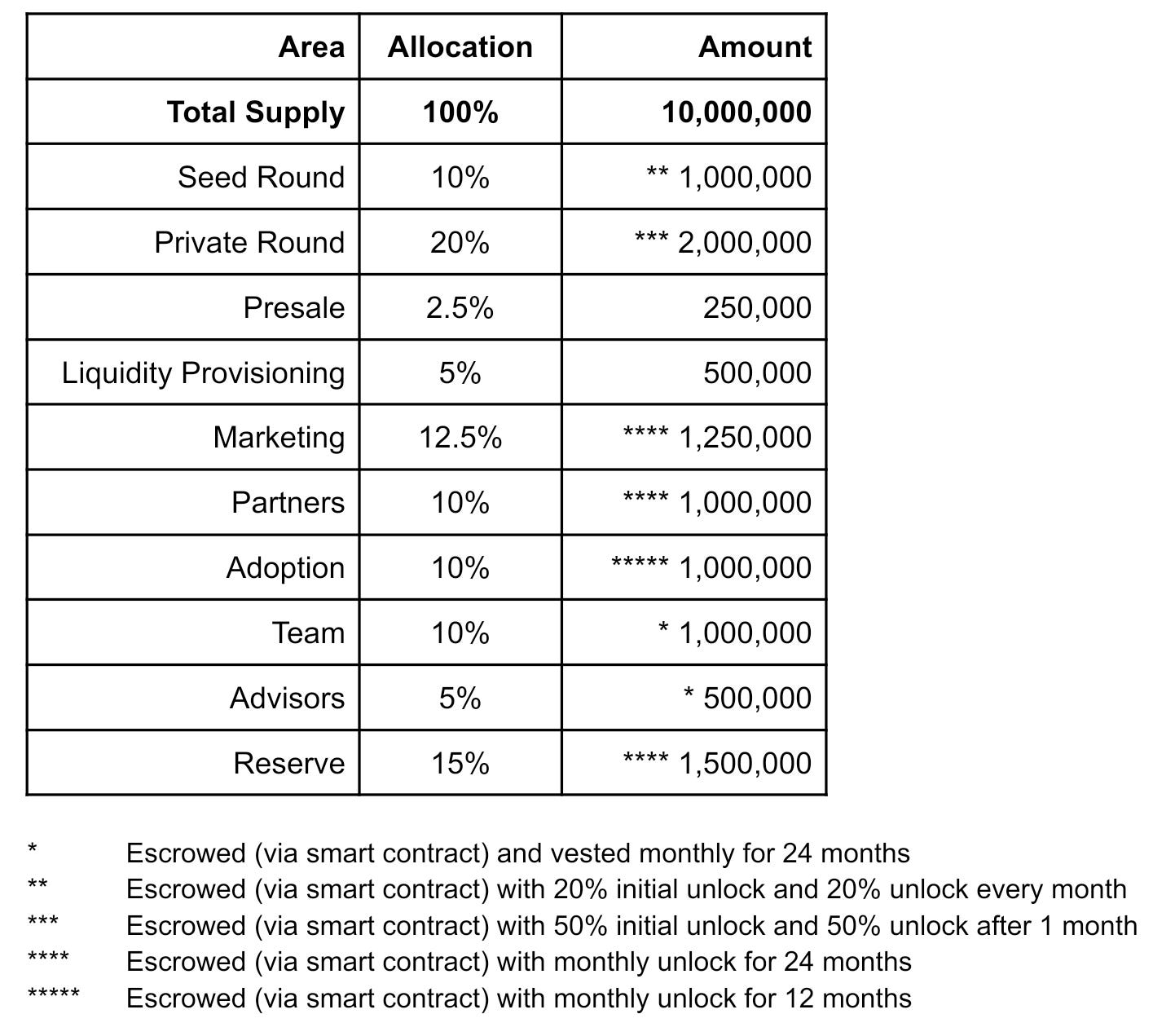

Token allocation

Looking for more information…

☞ Website ☞ Social Channel ☞ Social Channel 2 ☞ Message Board

Would you like to earn LDFI right now! ☞ CLICK HERE

Top exchanges for token-coin trading. Follow instructions and make unlimited money

☞ Binance ☞ Bittrex ☞ Poloniex ☞ Bitfinex ☞ Huobi

Thank for visiting and reading this article! I’m highly appreciate your actions! Please share if you liked it!

#blockchain #bitcoin #lendefi #ldfi